- “Eight of the 14 components meet all minimum provisions of the relevant Basel standards and these were therefore graded as "compliant".”

- “Four of the components were assessed as "largely compliant", reflecting the fact that most but not all provisions of the global standard were satisfied.”

- “One component - the Internal Ratings-based (IRB) approach for credit risk - was assessed "materially non-compliant" and pertained primarily to the treatment of exposures to SMEs, corporates and sovereigns.” In particular, the report notes that exposures to SMEs are given concessionary risk weightings, presumably to try to encourage this specific type of lending, however it is nonetheless not in line with the rules. Furthermore, it finds that banks are given a significant amount of leeway in how to value their sovereign debt holdings, with most across the EU simply applying zero-risk weighting – again this is a deliberate attempt to limit any distortions to the sensitive Eurozone government debt markets.

- “Another component was found to be "non-compliant". This relates to the EU's counterparty credit risk framework, which provides an exemption from the Basel framework's credit valuation adjustment (CVA) capital charge for certain derivatives exposures.” Essentially the current rules allow exemptions for instruments which are not traded on exchanges or the wider market and therefore may be hard to value. Furthermore, this “materially boosts bank capital ratios,” though the report accepts that the EU is considering changes to these specific rules.

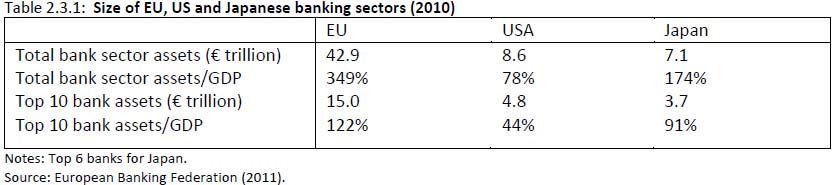

- Overall the EU was given the second lowest rating (on a scale of four) of “materially non-compliant”, making it the first jurisdiction to be found on the whole not the be complying with the Basel rules. The assessment is also particularly poor compared to the US, which was found to be “largely compliant” with the rules, in general its failings also seem to be more minor as well as less numerous.

While all of this may seem rather mundane and technical it does have some important implications.

First off, it raises questions about the quality and thoroughness of the recent ECB and European Banking Authority stress tests. We, along with plenty of others, have already raised concerns about this and the report adds further weight to those concerns. Furthermore, the specific problems outlined would certainly have helped present European banks as having higher capital ratios largely by reducing the perceived riskiness of certain assets they hold.

A report by Yalman Onaran for Bloomberg earlier this week highlighted the problems relating to the use of banks internal models to weight risk by contrasting this approach to that of using the pure leverage ratio. As the article notes, under the leverage ratio approach 12 large European banks would need to raise a further €66bn in capital. While neither approach is perfect, the Basel Committee’s indictment of the bank’s internal models and the way a large number of exposures in a number of sectors are valued seems to support such analysis and criticisms.

The second important implication is that is once again clearly highlights that the EU probably remains the more important level of policy making and legislation than international level or international organisations – at least when it comes to how things are structure on the ground.

Despite agreeing to follow the Basel III rules the EU is the one that designs and implements the specific legislation. In this case it has clearly altered the rules significantly to suit its own needs – the gap with the original rules as well as how they are interpreted and implemented in other jurisdictions is clear. Furthermore, while the Basel Committee can issue a damning judgement of the EU’s approach, it cannot force it to change. In this relationship all the hard (legal) power lies with the EU. This also extends beyond just implementation to interpretation. Despite writing the Basel III rules the Basel Committee is not even able to guarantee primacy on how they should be interpreted as the EU’s response to the report clearly shows.