The summary of the analysis is:

There are a few reasons why we believe the Cypriot bailout is unlikely to end particularly positively for the eurozone. Firstly, the usual methods of cutting the debt burden and/or taxpayer contribution such as bank or sovereign debt restructuring are very tricky to enforce in Cyprus (see table below, click to enlarge):Though progress has been made, eurozone finance ministers are unlikely to reach a final deal on the Cypriot bailout at their meeting this evening. Even if they do, any deal is likely to be another fudge, shying away from more radical options such as significant bank restructurings or depositor write downs. Amid political resistance in Germany and elsewhere to another bailout, eurozone leaders will seek to shrink the size of the €17bn bailout by up to €7bn. However, we estimate that even in a best case scenario, only around €4.5bn could realistically be cut, due to practical and political constraints. This will leave Cypriot debt to GDP at 130% - a level that remains wholly unsustainable. In turn, this makes further financial assistance for Cyprus likely, reminiscent of developments in Greece.

Fundamentally, the row over Cyprus – which accounts for only 0.2% of Eurozone GDP – illustrates that firstly, three years into the eurozone crisis, the block still has no effective tools to restructure debt and repair banks amid the complicated politics of the eurozone. Secondly, the stand-off between the creditors in the eurozone north and the austerity-fatigued south could well be hardening.

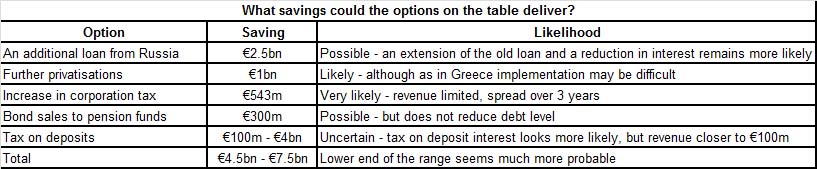

Secondly, the alternative options on the table simply do

not deliver enough savings (at least not without the risk of significant

contagion which politicians are likely to shy away from):

That leaves us with a very familiar solution: another fudge.

In terms of what to expect from tonight's meeting, well, probably no conclusive deal for a start. At best an agreement on some of the options above. The audit of Cypriot anti-money laundering regulations is just beginning and the final result will likely play a role in determining the level of conditions Germany applies to the bailout. (As the WSJ noted recently, the institution running the audit has previously ranked Cyprus above Germany in terms of its rules on money laundering, so exactly how much the result will help remains unclear).

See here for the full piece.

4 comments:

Debt that can't be paid back won't be paid back - is still true even if the debt is bonds issued under UK law. Therefore it should be possible to include those bondholders in financing the Cyprus bailout.

Depositors who hold more than the guaranteed amount are at this stage not only depositors. Anything over the guaranteed amount is to be seen for what it is: an investment. In addition: for foreign depositors, if it was only deposits why would they keep money over the guaranteed amount in a bank in a foreign nation? Investment reasons.

The people of Europe deserve better from their "leaders".

A monkey with a pin would have done a better job resolving this and would be far more trustworthy with it.

Can we vote for a monkey? Sorry, I forgot that we are not allowed a vote.

Having seen the bailout figures this morning, it is not enough to pull the Cypriot economy back to stability. This measure is just another temporary political screw up that perpetuates the EU/Eurozone disaster.

The politicians of Europe are lying to the people AGAIN and must be brought to account via the courts when this is over. Life sentences, sequestration of assets and public hangings apply to these incompetents.

Probably the tax on the bankdeposits is not allowed under taxtreaties Cyprus has concluded.

At least for deposits held by inhabitants in those taxtreaty countries.

Post a Comment